It’s About The Patient, Dummy!

Ascension St. Vincent Dunn in Indiana; Franciscan Health in Indiana; Saint Luke's Community Hospitals in Olathe and Shawnee; Cleveland-based St. Vincent Charity Medical Center; Hazel Hawkins Memorial Hospital in California; Wellstar Health System’s downtown Atlanta Medical Center; El Segundo, California-based Pipeline Health System; Berwick Hospital Center in Pennsylvania; Blessing Health System’s hospital in Keokuk, Iowa; Borrego Community Health Foundation in Borrego Springs, California; Community Health Systems’ ShorePoint Health Venice, Florida; Santa Cruz Valley Regional Medical Center in Green Valley, Arizona; Patients' Hospital of Redding, California; Wellstar Health System’s Atlanta Medical Center South; Cleveland (Texas) Emergency Hospital; Audrain Community Hospital in Mexico; Montana, and Callaway Community Hospital in Fulton, Montana; Brandywine Hospital in Coatesville, Pennsylvania; Jennersville Hospital in West Grove, Pennsylvania; Galesburg (Illinois) Cottage Hospital.

These are the 19 hospitals that filed for bankruptcy, closed or announced plans to close last year. And the tough times continue in 2023. For 2nd Quarter this year, for-profit “Community Health Systems” reported a net loss of $38 million.

For 2nd Quarter this year, for-profit “Community Health Systems” reported a net loss of $38 million.

This summer, Intuitive Surgical, the leading manufacturer of surgical robotic instruments also reported their 2ndQuarter financial results. Revenues were up 15% year-over-year to 1.76 billon dollars. They expect their gross margin for 2023 to be between 68 and 69%.

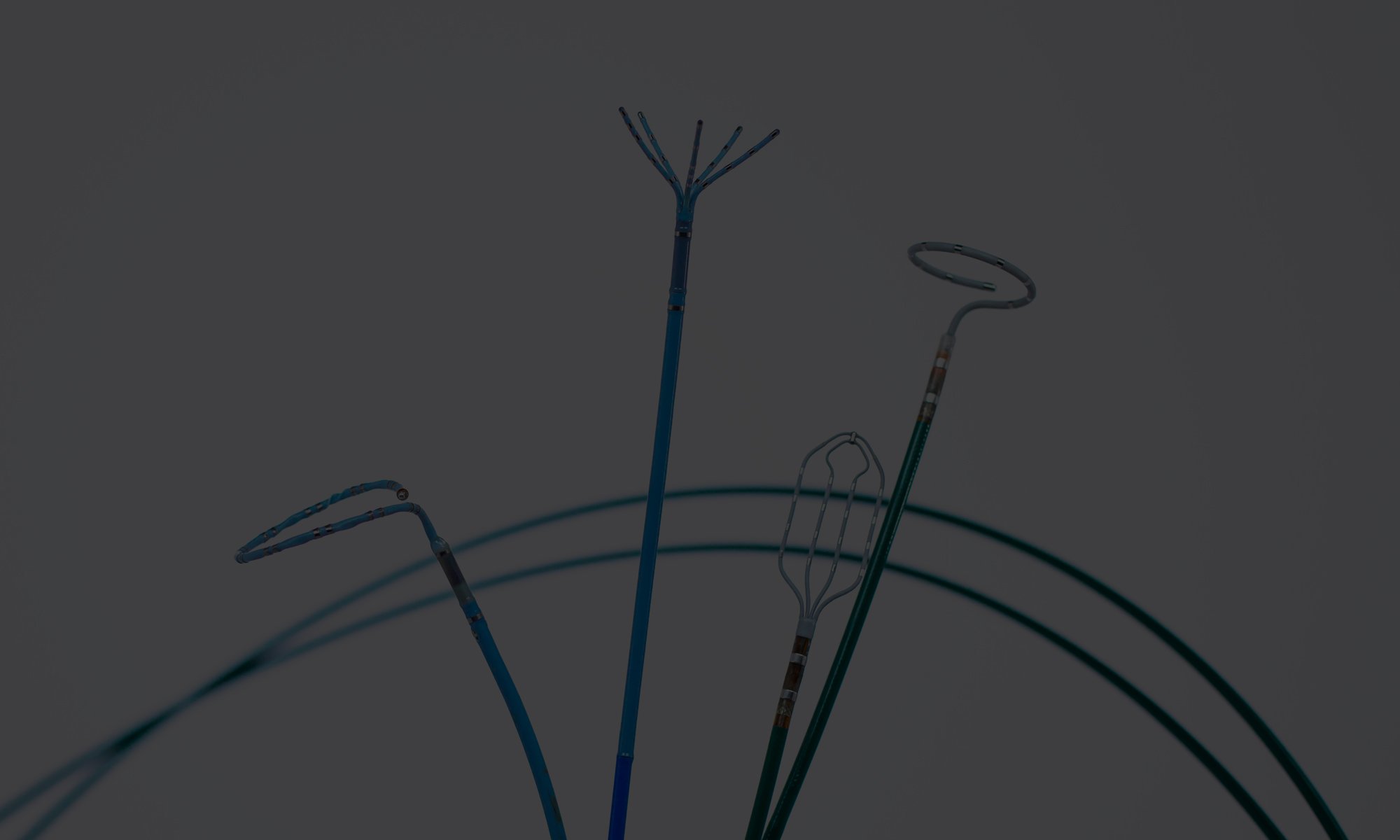

In electrophysiology, Biosense Webster’s sales of electrophysiology devices were up 26% in the 2nd Quarter, and Abbot, another manufacturer of electrophysiology devices, saw sales grow by 17%.

Biosense Webster’s sales of electrophysiology devices were up 26% in the 2nd Quarter, and Abbot, another manufacturer of electrophysiology devices, saw sales grow by 17%.

There are winners and losers in all markets and industries. But when technology manufacturers win big and hospitals lose big, the real loser is not the shareholder or the hospitals administrator – he or she can probably find another job – the real loser is the patient.

In electrophysiology, manufacturers’ costs go up 10% per year between price increases and launch of new products at a higher price level. Reimbursement does not. In her October 2019 article, “Change and Challenge: Understanding the Finances of the Electrophysiology Lab”, Corazon consultant Carol Wesley pointed out that “reimbursement rate increases in general are often below inflation rates, and do not keep pace with the rising costs of EP’s advanced technology and devices.”

She continues, “Our clients are continually looking for ways to solve the high-quality/low-cost equation without sacrificing patient access. Understanding the economic impacts on the EP lab can lead to more informed decision-making and better strategies for the future of this dynamic subspecialty.”

However, the economics are actually very easy to understand: When prices keep going up and revenue (reimbursement) goes up by less, procedure profits head towards zero and beyond. There are, of course, several things the hospital can do when revenues can’t keep up with costs. They can address process flows, operational inefficiencies, reduce staffing and labor costs, or improve quality to reduce re-admissions. But most hospitals today have reduced their staffing to the absolute minimum and implemented every operational efficiency available - to the point where the engine simply cannot run any leaner.

When prices go up disproportionate to reimbursement, the simple reality is that the labs must reduce costs somewhere else. It’s a zero-sum game. If they don’t do that, the lab will start losing money on procedures. When a hospital service line loses money, hospitals in reality must consider closing down that service line. When a service line, such as an electrophysiology lab closes, this means patients will be unable to have procedures. The patient always pays in the end, when the hospital math doesn’t work out.

The patient always pays in the end, when the hospital math doesn’t work out.

This is the bottom line: Electrophysiology labs will not fix the cost-income problem without addressing how medical devices and instruments are used. This means reducing waste in the supply chain, it means demanding manufacturers design reusable products or products that can be reprocessed, it means maximizing reprocessing savings (which can reduce device costs by 30% per procedure), and it means using advanced instrument repair companies to ensure the lab is not unnecessarily purchasing new equipment.

These are examples of deliberate resource utilization, and it is a critical strategy in the hospital’s ability to remain profitable, sustainable, and provide the best possible care for as many patients as possible.